Charitable/religious

trusts are the trusts which are formed with an objective of providing relief to

poor, education ,medical relief, preservation of environment/ monuments ,

advancement of objects of general public utility, religious purpose, etc. There

taxation has always been a point of concern. The entire income of such trust(be

it house property, capital gain or any other income) is taxed as per the

provisions of section 11-13 of the Income Tax Act ,1961 rather than as per

there relevant provisions . Here I have discussed the major areas related to

taxation of income of such charitable/religious trusts.

Income

of charitable/religious trust can be classified as follows:-

I. Voluntary Contributions(donations) Section 11(1)

Voluntary

contributions are basically the donations received by the charitable/religious

trust which form part of income of the trust.

They

are of two types:

1)

Donations received with specific direction that they shall form part of corpus

fund

Such

donations are exempt

2)

Donations received without such specific instruction

Such

donations shall form part of income from trust property

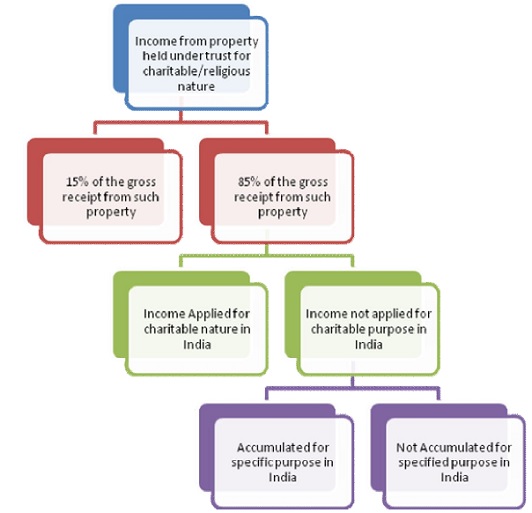

II. Income From Property held under trust for charitable and

religious purposes

Particulars

|

Taxability

|

||||||||||

15%

OF GROSS RECEIPTS FROM SUCH TRUST PROPERTY

|

EXEMPT

|

||||||||||

85%

OF GROSS RECEIPT FROM SUCH TRUST PROPERTY

|

|||||||||||

i.

Income Applied For charitable Purposes in INDIA

|

EXEMPT

(Sec11(1))to the extent to which applied for the following purposes:

1. Purchase of capital asset

2. Repayment of loan for

purchase of capital asset

3. Revenue Expenditure

4. Donation to trust registered u/s

12AA or u/s 10(23C)

|

||||||||||

Income

DEEMED TO BE APPLIED FOR CHARITABLE

PURPOSE

IN INDIA:

IN CASE WHOLE OR PART OF INCOME IS NOT RECEIVED DURING

THAT YEAR IN WHICH IT IS DERIVED

|

-Exempt

in case :

a. Income is applied for charitable purpose in India in

the year of receipt or in the immediate succeeding year.

b. Assessee submits a declaration to the Assessing Officer

on or before the due date of filling of return as per section 139(1) that

such income shall be applied for such purpose in the year of receipt or

succeeding year.

|

||||||||||

IN

ANY OTHER CASE

|

-Exempt

in case :

a. Such income is applied in abovementioned charitable

purposes in the immediately succeeding year.

b. Assessee submits a declaration to the Assessing Officer

on or before the due date of filling of return as per section 139(1) that

such income shall be applied for such purpose in the immediate succeeding

year.

|

||||||||||

II.

INCOME NOT APPLIED FOR CHARITABLE/RELIGIOUS PURPOSE IN INDIA

Q) What are the modes in which income shall be

accumulated for specific purpose (sec 11(5))??

A) 1. Investment in government saving certificate/UTI

2. Deposit in post office savings bank/scheduled bank.

3. Investment in immovable property.

4. Deposit with or investment in bonds of a public co.

having main object of providing long term finance

for urban infrastructure/industrial development/

residential house, in India

|

A) ASSESSEE GIVES NOTICE TO

Assessing officer specifying purpose and period

(cannot exceed 5 years) of accumulation before assessment is complete.

B) Accumulated amount is

deposited /invested in specified form.

|

||||||||||

Not

accumulated for specific purpose in India

|

Taxable

in case income is not applied for charitable/religious purpose in India and

is also not accumulated for specific purpose in India.

|

III. CAPITAL GAINS (Sec 11(1A)

The

capital gain arising from the transfer of a property held by

religious/charitable trust shall be taxable as under:

1) Cost of new asset ≥ net

consideration from asset sold → Entire capital gain is

exempt

2) Cost of new asset < net consideration

from asset sold → Capital Gains Exempt = Cost of new asset less

Cost of old asset

IV.

Anonymous Donations (Sec 115BBC)

Q)

What are anonymous donations??

A)

Anonymous donations are basically the donations where the person receiving the

donations doesn’t maintain any record of the person giving the donation. E.g. –

Offerings given in temple in donation box.

Taxability

Step

1: Compute the total amount of anonymous donation received by the

charitable/religious institution

Step

2 : Compute 5% of the total donations(corpus donations + anonymous donations +

other donations not forming part of corpus)

Step

3 : Select the higher of the following two:

a)

Amount computed in step 2 or

b)

1,00,000

The

amount computed in step 3 shall be exempt and the remaining amounts of

anonymous donations are taxable in the hands of such charitable/religious institution

@ flat 30% (115BBC)

Cases where anonymous donations shall not be taxable u/s

115BBC

1)

Where donations are received by trust established WHOLLY for RELIGIOUS purpose

(no charitable purpose). E.g.-donations given by devotees to trust owning a temple.

2)

However in case such religious/charitable trust also runs a school/medical

institution/educational institution ,etc and the donations are received with

specific direction that they are for such school/institution then such

donations shall be taxable

Anonymous

donations not taxable u/s 115BBC → taxable as per section 11 & 12

Anonymous donations taxable u/s 115BBC → not exempted u/s 11 & 12

Section 13: Section 11 not to apply in certain cases:

1.

Entire income from the property held under a trust for private religious

purposes which does not enure for the benefit of the public.

2.

Entire income of a charitable trust or institution created or established for

the benefit of any particular religious community or caste.

3.

Entire income of the following charitable/religious trust:-

a) where any part of the income of such trust is used for the benefit of any

person specified under sec13(3) or

b) Where any property of the trust id used for the benefit of any person specified

under sec13(3)

4.

Entire income of a charitable /religious trust whose funds are not invested in

modes specified under section 11(5).

-

See more at:

http://taxguru.in/income-tax/taxation-charitablereligious-trust.html#sthash.pzFJZTQb.dpuf

{kind=link}

No comments:

Post a Comment